Buy now, pay later (BNPL) is booming across Asia Pacific, at a time when Covid’s impact has turbo-charged demand for e-commerce and new types of credit. If trends continue, the BNPL industry in the Asia-Pacific region could exceed US$133.69 billion by the end of this year.

But this could be the tip of the iceberg. While BNPL offerings are mature in Australia and New Zealand, due, in large part to the emergence of Afterpay, countries in South East Asia have new markets with room for incredible growth.

Of course, as is the case with BNPL across the globe, regulation could impact its trajectory. But the payment method is already truly embedded in the digital economy and is not going anywhere, even if it is regulated.

Let’s look at the conditions that were so favourable to this payment method, the inevitable regulations and consumer and media response.

BNPL is disrupting credit and driving competition

Apac has always been a dynamic region, with a reputation for disruptive innovation, especially in payments. It’s no surprise that BNPL has taken off at speed – giving rise to a highly competitive market.

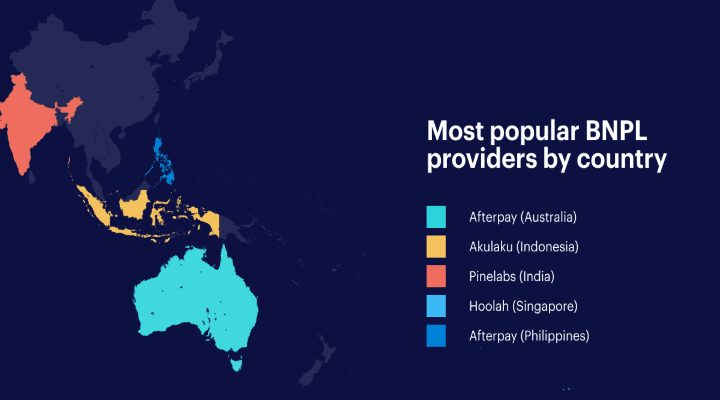

In Australia and New Zealand, Afterpay dominates. This is unsurprising as it is an Australian company. In fact, in Australia, almost three out of four Australians are aware of BNPL as a payment option and 70 per cent of consumers are aware of Afterpay. In comparison, a competitor, Zip, was known to 50 per cent of consumers. Australia is regarded, along with Sweden, Germany and Denmark as one of the top countries for BNPL.

Elsewhere across the region, smaller local players and fintech start-ups are coming to the fore. These include of Pine Labs in India, Akulaku in Indonesia, Cashalo in the Philippines and Hoolah in Singapore.

Incumbent banks are also muscling in on the act, though, by launching their own interest-free BNPL solutions on top of their existing credit card offerings. Similarly, e-commerce platforms and retailers are looking to garner a slice of the market with their own low or interest-free instalment-based plans and loyalty programs. Some of the big BNPL players are established super apps like Grab, Gojek and Alipay.

All these players are promoting BNPL heavily and fueling consumer awareness and adoption. With penetration in some markets now reaching double figures, credit businesses are seeing this eat into their customer base. Particularly as younger Apac audiences make the switch or move straight to BNPL in cases where they are not able to access more traditional forms of credit.

And, with BNPL options available through super apps like Grab, this payment option is far more accessible. Grab’s Pay Later service, for example, is available through the GrabPay Wallet giving customers more choice at the checkout.

Additionally, many players in this space are very data-driven and so are able to give customers the options that they want and market these options to them in the right way. Hoolah is a great illustration of this as the company uses its data-driven approach to be agile in how they address and fix customer problems.

Asia and Southeast Asia will see explosive growth

The presence of home-grown brands like Afterpay has pushed New Zealand and Australia further ahead of the Apac curve. But as these BNPL markets mature, attention is turning to opportunities in Asia and Southeast Asia. Here, there are some unique drivers that make BNPL a natural next step for payments.

Among these are:

- High volume of spending power

Apac has some of the biggest and fastest-growing consumer markets in the world. By the end of the decade, Asia alone will represent half of the world’s consumption growth – a $10 trillion opportunity. Finding ways to empower people here to buy will become a top priority for businesses and brands looking for rapid growth. - Mid and low-tier sectors are ripe for credit

BNPL is empowering shoppers in mid-markets, e.g. consumer electronics, and in high-volume retail segments that traditionally don’t offer credit e.g. cosmetics which is a huge market in Asia. You can now buy makeup on instalment plans with the likes of Sephora. - Digital savvy but underbanked consumers

Although mobile and internet enabled, the region’s population is still underserved when it comes to financial services. Southeast Asia, for instance, has 670 million consumers, but only 27 per cent have bank accounts. BNPL helps fill the gaps by offering low-friction, instant credit that can be settled over time using prepaid digital wallets or other non-bank payment rails. - Bulk buy culture

In Southeast Asia, volume-selling is big business. From nail salons to air-con servicing, merchants prefer to sell packages or bundled services instead of one-off products. Bulk buying is traditionally funded using old-school POS financing or credit cards. BNPL is a natural alternative, making multi-purchasing more affordable, fee-free for customers and easier to access online.

Growth and power warrant more responsibility

There’s no doubt that BNPL is a disruptor and opens the door to new opportunities to help customers buy what they want when they want. But that’s not always good. Apac faces the same concerns around unregulated BNPL plans as Europe and MENAP.

How to protect young or financially illiterate people from misusing BNPL, overspending and incurring too much debt, is the focus of many government and regulator conversations.

There are clear signals that the regulatory approach for BNPL schemes will be reviewed as the use of BNPL in Apac continues to grow. For instance, last year the Australian Finance Industry Association (AFIA) launched a new BNPL Code of Conduct. Although falling short of regulation, 95 per cent of providers in Australia have already signed up.

More concrete industry guidelines on credit assessment, payment authorisation, and marketing practices are expected. Until then, uninformed consumers will be at risk from under-funded and irresponsible providers eager to exploit the market.

Find a trusted provider to keep on the right side of regulations

To safeguard themselves, Apac merchants should make sure they choose a reputable BNPL provider. Taking care to check out their credentials and track record as well as performance indicators and payback rates.

This should also include what data they’re using to understand their users and how they’re helping to educate them about responsible borrowing.

With Apac’s consumption engine primed and ready to go, navigating a trusted route to BNPL will be vital to long-term retail success.

Download the guide here and discover the impotence of switching to the right payment methods.